U.S. citizens, green card holders, and those who have been assigned to work in the U.S. as an expatriate are usually required to file their tax returns annually to the U.S. tax authority, the Internal Revenue Service (IRS).

When you are filing a return, it is very important to know if you are a U.S. resident or a non-U.S. resident.

That’s because U.S. residents and nonresidents have very different ways of taxation.

Under U.S. tax law, an individual is firstly classified as a “U.S. citizen” and “Alien”, and depending on the resident status, the alien is classified as Resident Alien and Nonresident Alien.

- “U.S. citizens” will be taxed on all income (worldwide income), regardless of where they live.

- Like U.S. citizens, “U.S. resident alien” will be taxed on all income they earn worldwide, including source income outside the United States.

- For “U.S. nonresident alien”, only U.S. source income is subject to U.S. taxation.

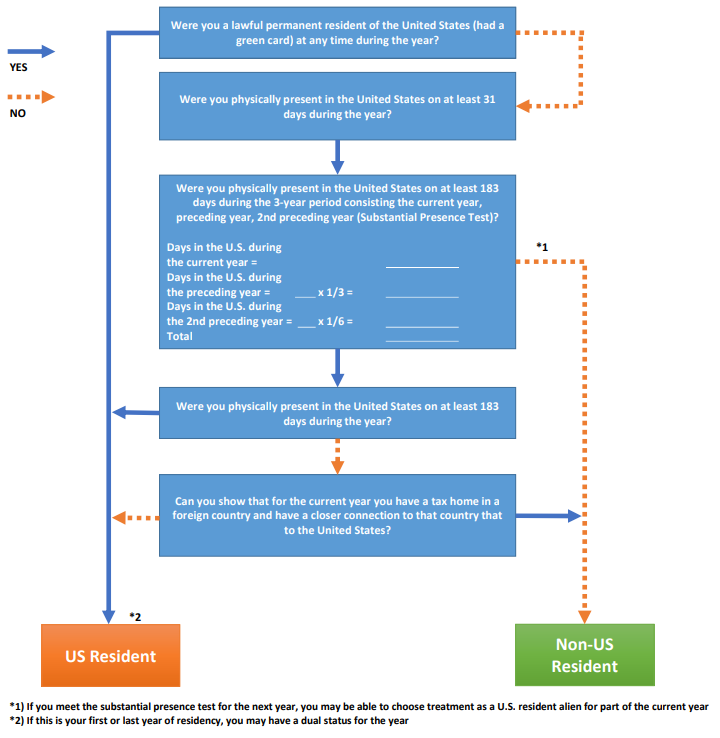

Judgment of U.S. Resident and Nonresident

The distinction between U.S. resident and nonresident for U.S. taxation is not simple. You cannot simply consider you as a “U.S. resident” if you live in the United States or “U.S. nonresident” if you do not live. It is determined by the following criteria:

First of all, those who hold a permanent residence (“Green Card”) during the year are regarded as U.S. residents regardless of the length of their stay in the United States.

Next, for the criteria above, when you count the number of days you stay in the U.S., in general, the date of entry to the United States and the date of departure from the United States are also treated as the date of stay in the United States, respectively.

When you determine your residency with the substantial presence test, if the result of the calculation includes any fraction, the fraction will be rounded off after adding all numbers.

In general, A, F, G, J, M, and Q visa holders are called Exempt Individual, and the length of stay in the United States while holding these visas are not counted for the substantial presence test purpose until a certain number of years.

Tax Home and Closer Connection

Even if you are treated as a U.S. resident as a result of the substantial presence test, you can still treat you as a U.S. nonresident if you meet the following conditions:

- Days of Presence in the U.S. is less than 183 days in the year

- Have a Tax Home outside the U.S. in the year, and

- Establish a closer connection to a country with tax home than the United States during the year

While the definition of Tax Home is complex, it can generally be thought of as the primary business location.

Under these conditions, in order to be considered as a U.S. nonresident, you must have Tax Home for the same country outside the United States through the year.

The following criteria are used to determine closer connection, and you must submit a Form 8840 when you file your tax return:

- The country of residence you designate on forms and documents

- The types of official forms and documents you file, such as Form W-9, Form W-8BEN, or Form W-8ECI

- The location of:

- Your permanent home

- Your family

- Your personal belongings, such as cars, furniture, clothing, and jewelry

- Your current social, political, cultural, professional, or religious affiliations

- Your business activities

- The jurisdiction in which you hold a driver’s license

- The jurisdiction in which you vote; and

- Charitable organizations to which you contribute

“Permanent Home” means a residence where you are not set up for a short stay, such as a trip or business trip, but for any other purpose to stay continuously.

Dual-Status Alien

If the filing year is a mix of U.S. resident and nonresident periods, it will be treated as Dual-Status Alien.

Dual-Status generally applies to the year you enter or leave the United States.

For example, if you are treated as a U.S. resident in the first year of your arrival in the United States, you will need to report your worldwide income after the date of entry as a resident.

You will be treated as a U.S. resident from the date of entry, and before that, you will be treated as a U.S. nonresident.

Therefore, income earned outside the U.S. before entering the U.S. is not required to be reported in the United States.

When treated as Dual-Status, the following restrictions apply because you are not a U.S. resident for the entire year:

- Standard Deduction cannot be used

- Head of Household and Joint Return are not allowed

- No Tax Credits, such as Education Tax Credit

First Year of U.S. Residency

If you become a U.S. resident for the current year and you were not a U.S. resident at any time in the previous year, you will only be treated as a U.S. resident for the period after the start date of the U.S. resident period.

If you meet the requirements for the substantial presence test and are treated as a U.S. resident, the U.S. resident period start date will be the first day you are present in the United States in that year.

10-Day Rule

However, you can exclude up to 10 days of actual presence in the U.S. from the start date of the U.S. resident period if the following conditions are met:

- Your Tax Home was in a foreign country, and

- You had a Closer Connection to that country than to the United States

This 10-day rule is generally used by expatriates who come to the U.S. for short-term business trips or home searches before they are assigned to the U.S., and the following rules apply when excluding 10 days:

- You can exclude days from more than one period of presence as long as the total days in all periods are not more than 10,

- You cannot exclude any days in a period of consecutive days of presence if all the days in that period cannot be excluded

- Although you can exclude up to 10 days of presence in determining your residency starting date, you must include those days when determining whether you meet the substantial presence test

As an example, if you have a short-term business trip to the U.S. from January 6 to January 10, and you move to the U.S. on March 1 and resided for the rest of year, you can exclude a total of five days from January 6 to January 10, and it means that your U.S. resident period start date is March 1.

In addition, when applying the 10-day rule, it is necessary to attach a statement with the necessary information on your tax return.

U.S. Residency Starting Date for Green Card Holders

If you have a green card during the year and do not meet the substantial presence test requirements, the U.S. resident period start date will be the first day you are present in the U.S. as a green card holder.

On the other hand, if you have a green card during the year and meet the conditions of the substantial presence test, the start date of the U.S. resident period will be the earlier of the first day you are present in the United States as a green card holder or the first day you are present in the United States under the substantial presence test.

U.S. Residency During the Preceding Year

If you are a U.S. resident for any period of the previous year and are a U.S. resident during any period of the current year, you will be treated as a U.S. resident as of January 1 of the current year.

For example, let’s say that you stay in the U.S. as a U.S. resident between May 1 and November 5 of the previous year, then return to Japan and move to the U.S. as a green card holder on March 5 of the current year.

In this case, the start date of the U.S. resident period for the current year will start from January 1 of the current year.

First Year Choice

For the first year, even if you do not meet the green card test and the substantial presence test, you can still file a tax return as a U.S. resident if you meet all of the following conditions.

- You are not a U.S. resident in current the year

- You are not a U.S. resident during the previous year

- As a result of the substantial presence test, you are considered as a U.S. resident for the following year

- Be present in the U.S. for at least 31 days in a row in the current year, and

- Be present in the United States for at least 75% of the number of days beginning with the first day of the 31-day period and ending with the last day of the current year. For purposes of this 75% requirement, you can treat up to 5 days of absence from the United States as days of presence in the United States.

The main point of this special treatment is that you satisfy the substantial presence test for the following year.

As of April 15, the normal filing deadline, you cannot prove that you will meet the substantial presence test for the following year.

Therefore, when making the first year choice, it is necessary to apply for an extension of the tax return filing deadline, extend the deadline to October 15, meet the conditions of the substantial presence test, and then submit the tax return before October 15.

In addition, in order to apply the first year choice, it is necessary to attach a statement with the necessary information on your return.

Election of Full Year U.S. Resident under 6013(h)

If you are treated as a Dual-Status Alien in the filing year, you can file your return as a U.S. resident for the entire period from January 1 through December 31 of that year if you meet all of the following conditions (6013(h) Election):

- You were a nonresident alien as of January 1 of the year

- You are a resident alien or U.S. citizen as of December 31 of the year

- You are married to a U.S. citizen or U.S. resident alien as of December 31 of the year

- Your spouse joins you in making the choice

If you make the 6013(h) election, you must attach a statement with the necessary information on your return.

Election of Nonresident Spouse Treated as a Resident under 6013(g)

If you have a marital relationship as of December 31 of the year, and one spouse is a U.S. citizen or U.S. resident and one spouse is a U.S. nonresident, you can choose to treat the nonresident spouse as a full-year U.S. resident (6013(g) Election).

If you make a 6013(g) election, you will need to file a join income tax return for the year in which you made the election, but after the following year, you can choose whether to file joint or separate returns.

If you make a 6013(g) election, you must attach a statement with the necessary information to your return.

Please note that if one spouse is substantially a U.S. nonresident, the spouse is not be able to obtain a social security number, so the spouse will need to apply for an ITIN (Individual Taxpayer Identification Number) when filing your tax return.

Last Year of U.S. Residency

If you are a U.S. resident for the year and you are not a U.S. resident at any time in the following year, you will be treated as a U.S. nonresident for the period after the end of the U.S. resident period.

The end date of the U.S. resident period is December 31 of the year, but depending on the following conditions, it is possible to start the period before December 31.

- Tax Home after the end of the U.S. resident period is located outside the U.S.

- You have closer Connection to the country than the United States after the end of the U.S. resident period

If the above conditions are met, the end date of the U.S. resident period will begin on one of the following days:

- The last day in the year that you are physically present in the United States, if you met the substantial presence test;

- The first day in the year that you are no longer a lawful permanent resident of the United States, if you met the green card test; or

- The later of the dates above, if you met both tests

In order to establish an end date for the U.S. resident period, a statement with the necessary information must be attached to your return.

De Minimis Presence

If you are treated as a U.S. resident because of the substantial presence test and you qualify to use the earlier residency termination date, you can exclude up to 10 days of actual presence in the United States in determining your residency termination date (De Minimis Presence rule).

The following rules apply when excluding 10 days in this De Minimis Presence rule:

- You can exclude days from more than one period of presence as long as the total days in all periods are not more than 10

- You cannot exclude any days in a period of consecutive days of presence if all the days in that period cannot be excluded

- Although you can exclude up to 10 days of presence in determining your residency termination date, you must include those days when determining whether you meet the substantial presence test

As an example, let’s look at a case where you move to the United States on March 1, return to your home country on August 25, stay in the U.S. again from December 12 to December 16 of that year, and be treated as a U.S. nonresident for the following year.

In this case, as a result of the substantial presence test, you will be treated as a U.S. resident after March 1 of the year.

In addition, if you have closer connection to your home country than the United States for the period after August 25, you can exclude five days from December 12 to December 16, and set the end date of the U.S. resident period to August 25.

U.S. Residency During the Next Year

If you are a U.S. resident during any part of the following year and you are a U.S. resident during any part of he current year, you will be treated as a resident through the end of the current year.

This provision applies even if you have closer connection to a country outside the United States than the United States during the year.

コメント